The Crucial Role of Semiconductors for Original Equipment Manufacturers (OEMs)

As modern vehicles increasingly embrace electrification and intelligence, semiconductors have become a cornerstone of competitiveness for Original Equipment Manufacturers (OEMs). By ramping up investments in semiconductors, OEMs are delving deeper into the supply chain to secure critical components necessary for electrification and advanced driver-assistance systems (ADAS).

Growth Trends in the Automotive Semiconductor Market

According to the latest Automotive Semiconductor Trends report, the global automotive semiconductor market is expected to grow from $52 billion in 2023 to $97 billion by 2029, representing a compound annual growth rate (CAGR) of 11%. This robust growth trajectory has garnered widespread attention from OEMs, driving their strategic initiatives to capitalize on the opportunity.

OEM Participation in the Automotive Semiconductor Sector

Direct involvement of OEMs in the automotive semiconductor domain is a relatively recent phenomenon. Traditionally, OEMs have relied on third-party suppliers for semiconductor needs. However, the supply chain disruptions during the COVID-19 pandemic revealed the vulnerabilities of this model, forcing some automakers to cut production or manufacture vehicles lacking critical chips. These lessons have spurred OEMs to prioritize supply chain resilience and invest in developing in-house chips to reduce dependence on external suppliers.

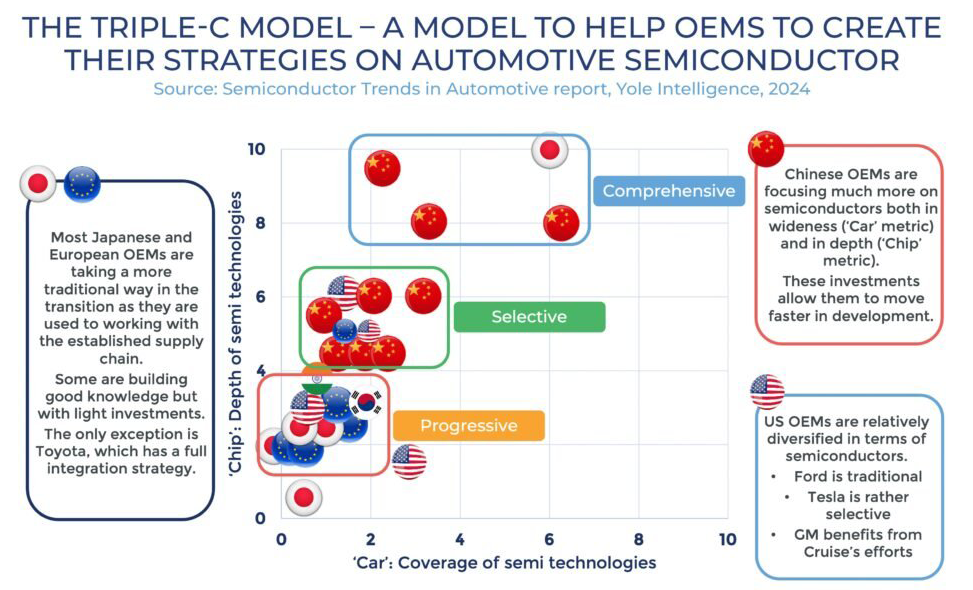

Yole Group’s CCC Model for Strategic Guidance

To aid OEMs in formulating effective semiconductor strategies, Yole Group introduced the CCC (Car, Chip, Confine) model:

1. Car (Automotive Semiconductor Technology Coverage): Evaluates the breadth of semiconductor technologies developed in-house by OEMs, encompassing critical domains identified in modern vehicles.

2. Chip (Depth of Semiconductor Technology): Analyzes the vertical integration depth of OEMs in the semiconductor space, ranging from fabless models to fully integrated device manufacturers (IDMs).

3. Confine (Supply Chain Localization and Resilience): Assesses efforts to enhance resilience and localization within the global supply chain.

By integrating these indicators, the CCC model provides insights into whether OEMs are engaging at the system level or committing resources to semiconductor design and manufacturing.

Regional Trends and Technological Investments

Chinese OEMs:

Chinese automakers are accelerating investments in semiconductors, focusing on both technology breadth (Car indicator) and depth (Chip indicator). For example, BYD, through its dedicated semiconductor subsidiary, has collaborated with TSMC and MediaTek to develop ADAS central controller chips and 4nm smart cockpit chips.

U.S. OEMs:

U.S. automakers exhibit diverse semiconductor strategies. Ford maintains a traditional supply chain approach, while General Motors leverages Cruise’s capabilities to develop autonomous driving chips. Tesla, on the other hand, focuses on designing proprietary full self-driving (FSD) chips, showcasing strong vertical integration capabilities.

Japanese and European OEMs:

OEMs in Japan and Europe generally adhere to traditional supply chain models and transition more conservatively. The exception is Toyota, which stands out with its comprehensive integration strategy encompassing R&D and production.

Core Technological Domains and Selective Investments

Yole Group advises OEMs to concentrate on core semiconductor components to establish future competitiveness. Key areas of focus include:

● Power Devices: Essential for vehicle electrification, with applications in inverters, converters, and onboard chargers.

● System-on-Chip (SoC): Critical for ADAS and cockpit functions, with rapidly growing demand driven by the shift towards smarter vehicles.

● Microcontroller Units (MCUs): Expanding from traditional uses to play pivotal roles in modern electrical and electronic (E/E) architectures.

Additionally, the proliferation of in-vehicle displays has increased demand for GPUs in infotainment systems. Advanced vehicles’ reliance on satellite data and extensive sensor arrays further underscores the need for robust semiconductor capabilities.

Success Stories and Future Outlook

Chinese electric vehicle manufacturer NIO has successfully developed its own ADAS SoC chips, while BYD has achieved breakthroughs in smart cockpit chips through partnerships. Tesla’s custom-designed chips for FSD systems illustrate the potential of tailored architectures to meet specific requirements. These examples highlight how selective investment and vertical integration are pivotal to success in the semiconductor space.

Notably, OEMs have largely avoided high-barrier-to-entry markets like memory and RF devices, which are predominantly geared toward the smartphone sector.

Conclusion

The electrification and digital transformation of the automotive industry have driven OEMs to take an active role in the semiconductor sector. This shift not only strengthens supply chain resilience but also enhances overall competitiveness. In the rapidly evolving market landscape, the combination of selective investments and technological depth will be critical for OEMs to secure a leading position.